- Markets

- Resources

- Company

")

Welcome to the New Era of AI-Driven Trading!

CAPEX and Devexa are shaping a new era of trading powered by artificial intelligence, where decisions are clearer, insights faster, and opportunities easier to act on.

Learn the Markets with a Trusted Expert

Access daily insights and educational content from Andreas Thalassinos, one of the industry’s most experienced market experts.

Your First Trades Are on Us, Risk-Free!!

Explore 5,000+ opportunities across commodities, forex, and stocks, with protection on your first trades.

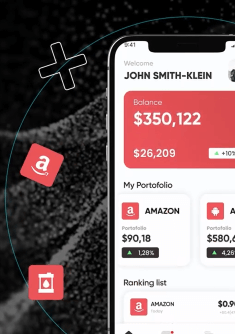

All-In-One

Options create

opportunities

Instant access to over 2100 leveraged products on FX,

indices, commodities, bonds, and more.

Capex

Academy

Tutorials, Analysis,

Charting, and Trends

Easy to use, packed with features. Analysis tools

from Trading Central, Insiders' Hot Stocks, Bloggers Opinions,

Daily Analyst Ratings, Hedge Funds Activity, and News

Sentiment from TipRanks.

- Instrument

- Buy

- Sell

- 30D Trend

On the move

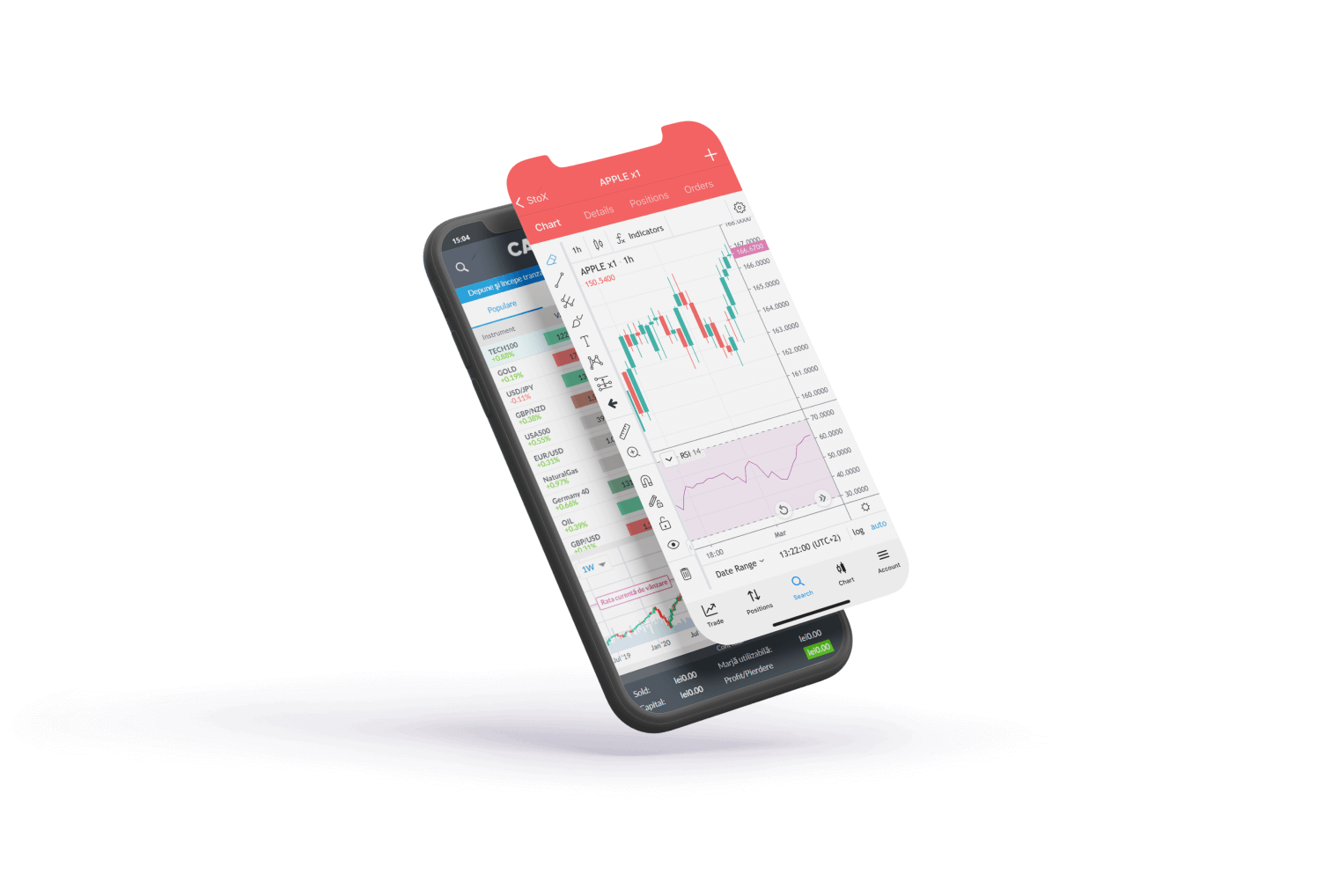

Fast and reliable trading, always connected, on our full-featured mobile app for phones or tablets, iOS and Android.

4.6

App rating

4.6

App rating

Why traders

choose

CAPEX.com

Security

Segregated bank accounts keep your money safe & separated from ours